Why We Avoid High-Growth Businesses

Atlasview Insights -- bite-sized weekly insights that are relevant to all business owners, dealmakers, and investors.

Welcome to Atlasview Insights! We are thrilled to have you join us for another edition packed with valuable content for small business owners, deal makers, and investors alike.

For those who may be unfamiliar with us, Atlasview Equity is a private equity firm specializing in software and tech-enabled businesses. To learn more about our experienced team and investment criteria, visit us here.

In this edition of our newsletter, we cover:

Atlasview Insights: Business returns vs investment returns

Deal Maker Perspectives

Our Favorite Reads

If you enjoy what you read, please be sure to subscribe and share with your colleagues.

P.s. we updated our website, and would love feedback!

Preferred Investment Criteria

We look for the following characteristics in our partner companies:

Industry: Software and tech-enabled businesses

Business Profile: Sticky B2B customer base

Size: Minimum $1m EBITDA or $5m ARR

Geography: The US & Canada preferred

Whether you’re a business owner interested in working with us, or an intermediary with a deal to share, always feel free to reach out and get in touch with us!

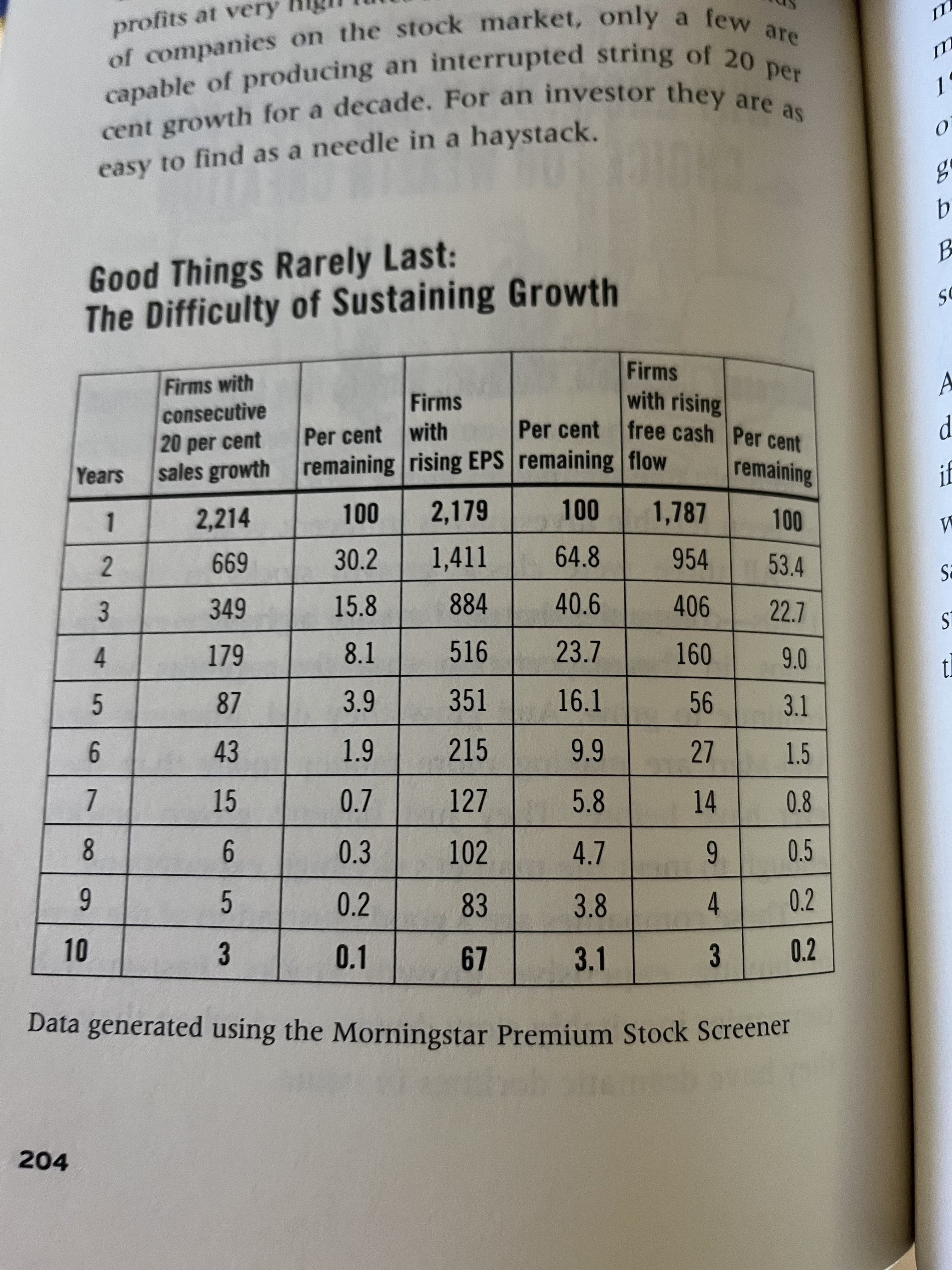

The Rarity of Sustained Growth

Below is a chart (from Seymour Schulich's book titled Get Smarter). which shows how rare sustained revenue growth:

There are several reasons why it's rare for a company to sustain revenue growth long term. Given the data above, as an investor, whichever company you are analyzing you can safely assume that it will not grow 20%/yr for 5+ years (let alone 10 years).

At Atlasview we generally avoid companies for sale that have experienced recent and rapid revenue growth, year over year. Here are a few reasons why:

Recency Bias

Most businesses that are "growing" 20%+ year-over-year probably have only done so for a year or two. If they had been growing 20%+ for any longer period, they wouldn't end up in Atlasview's universe of opportunities (small businesses), and instead, they'd be a much larger business. Why should we project or assume the company will continue to grow 20%+ during our ownership? According to the above data, this would be an improbable case. Brokers and sellers are quick to assign a valuation multiple on the most recent year, but if it's the business's best year ever, how do you know that the growth won't revert?

Lack of Cash Flow

The majority of "growth" opportunities we see are generally cash flow negative or break even at best. This is because everything is being reinvested back into growing revenues This heightens the risk profile of the business as the lack of cash flow reduces optionality. If the growth doesn't continue, you'll need to perform major cost reductions (which is not fun or easy). Or hope there is a greater fool to sell the business to, so you can realize your investment returns.

Unpredictable ROI

Plowing cash flow into organic growth has unpredictable ROI. Even if the growth appears profitable, it could still be destroying value depending on your cost of capital. As a PE buyer in the lower middle market, we have a high cost of capital, and therefore a high ROI hurdle rate.

Premium Multiple

This is the most important reason. Companies that are growing rapidly always trade for higher multiples. Investors take recent success/metrics and, often erroneously, project them out into the future. As a result, they justify paying higher multiples today for something they believe will happen in the future. We prefer not to operate in that regard, because the future is hard to predict. We believe in "making money on the buy" or having a margin of safety at acquisition. We achieve this by purchasing businesses on a reasonable multiple relative to the cash flow the business generates today.

If you’re an owner interested in working with Atlasview or an intermediary with a deal to share — feel free to reach out and get in touch with us. We will respond within 24 hours, and we can have an offer on the table within 7 days.

We are happy to pay referral fees for any deal referred and successfully closed.

Our Favorite Reads

📚 SMBs can be Freedom or a Prison: KPIs, People, and Accountability

Atlasview Insights <> Deal Bridge Media

This newsletter was powered by the team at Deal Bridge Media. Deal Bridge builds newsletters for M&A firms to help them generate more inbound deal flow.

Does your investment firm want to start a newsletter? Get in touch with Deal Bridge today!

Deal Maker Perspectives

About Us

Atlasview Equity is a private equity firm specializing in software and tech-enabled businesses. We combine patient capital with proven operational strategies to deliver predictable results for our stakeholders.